URD 2021

-

MESSAGE FROM THE CHAIRMAN AND CHIEF EXECUTIVE OFFICER

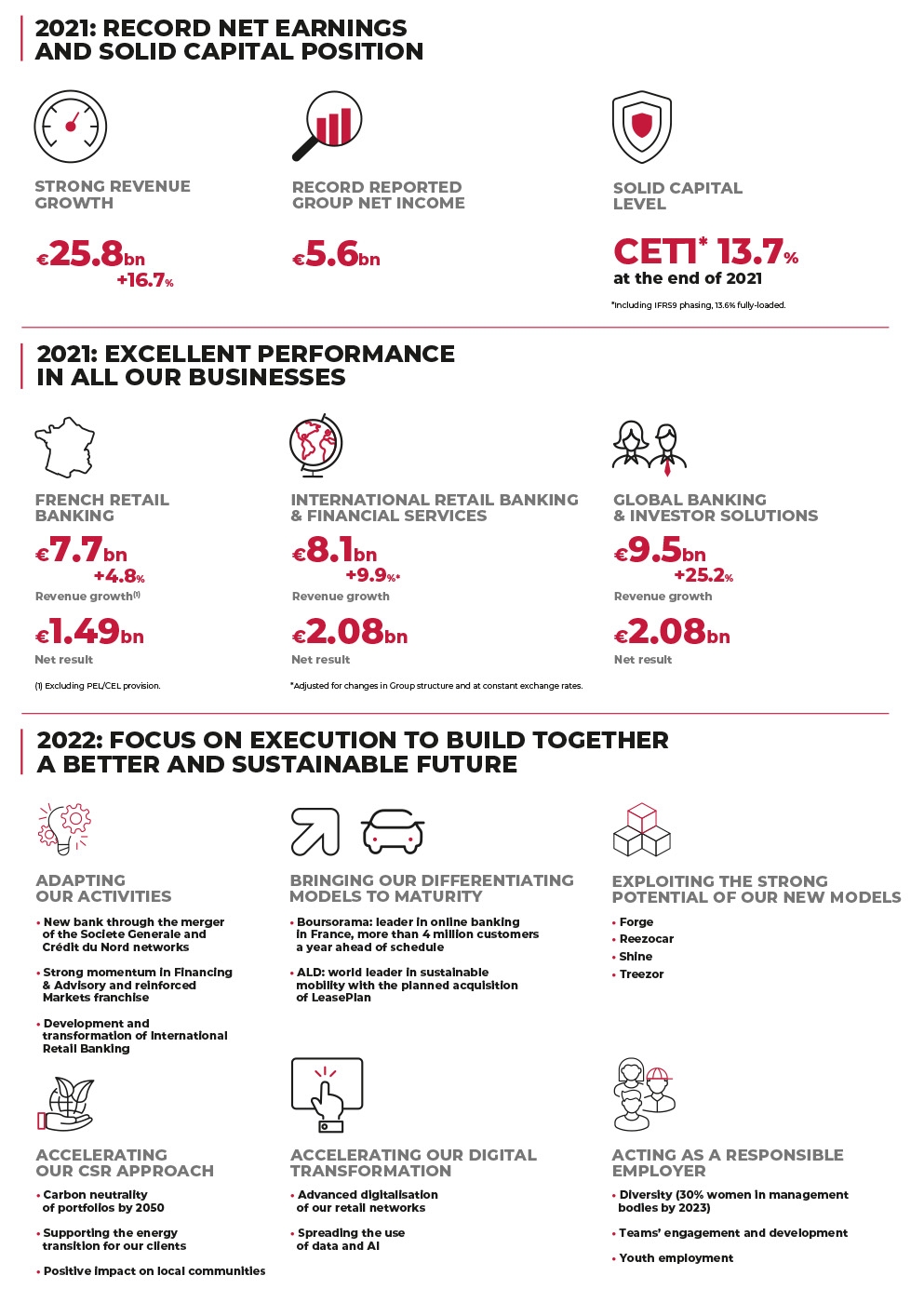

The year 2021 will be historic for our Group with the achievement of a record performance.

In 2021, beyond our ability to make the most of a situation favourable to economic recovery, despite the ongoing public health crisis, our financial and extra-financial performances confirm the coherence of our model, the solidity of our risk profile and the relevance of the strategy we are pursuing in each of our business lines. Societe Generale is a group that creates value for its clients, shareholders, staff and all of its stakeholders.

Record results

Above all, 2021 was a record year in terms of commercial and financial performance. Across all our business lines, we increased our revenues and kept costs and risks under control, resulting in a record high level of net income. The dynamism of our business lines was also demonstrated by the many significant transactions entrusted to us by our major clients, by the increase in our client satisfaction as well as the optimisation of the client experience and the services we offer, thanks in particular to our approach to digital innovation. Our Group has a very solid balance sheet, with a very high-quality loan portfolio and high capital ratios.

Strategic milestones

We also made progress with the roll-out of our major strategic projects in 2021, with ambitious objectives across all of our business lines and a constant focus on rigorous execution.

In Retail Banking in France, Vision 2025 – the project to merge the Societe Generale and Crédit du Nord networks – is now well advanced and will see the creation of a new bank from 2023, one with a commercially aggressive and more efficient model serving 10 million clients. At the same time, we are accelerating the development of Boursorama, the clear leader in online banking in France, driven by its outstanding client acquisition drive, with 800,000 new clients in 2021, and the additional benefits of the agreement signed at the start of 2022 to provide an alternative solution to clients of ING France. Boursorama is on track to achieve its target of more than four million clients a year ahead of schedule.

In International Retail Banking, Insurance and Financial Services, we finalised or continued our development plans for our international retail banking subsidiaries, as well as for our consumer credit activities. In Global Banking and Investor Solutions, we presented our new strategic roadmap focused on sustainable and profitable growth, with the ambition of building on our clients’ growing financing and advisory needs, and consolidating our market activities while continuing to manage our risk profile. Finally, in our specialist financial business lines, we are strengthening our banking and insurance model in all regions and moving forward with our plan for ALD to acquire LeasePlan, creating a world leader in sustainable mobility. We aim to close this transformative deal by the end of 2022.

Responsible banking commitments

In terms of ESG (Environment, Social, Governance), 2021 was also historic with our extra-financial performance recognised and welcomed by our stakeholders. Now equipped with a new ESG governance at Group level, we have reinforced our environmental commitments to achieve carbon neutrality in our business portfolios by 2050 and developed our positive-impact offers and solutions to support our clients’ energy transition, which we are actively supporting. As a responsible employer, we have made progress in achieving our objectives in terms of diversity and gender parity, as demonstrated by the recent appointments to the Group’s management bodies, and we continue to invest in our teams’ training and commitment levels. The end of the year also saw the definitive dismissal of the two legal proceedings initiated by the US authorities. We have completed the corrective action programmes and will ensure that the reinforcements of our compliance systems are incorporated over the long term.

Maintaining the momentum in 2022

In an environment set to be more volatile and uncertain, we are determined to sustain this positive momentum and maintain a regularly high level of results by combining commercial performance with a disciplined approach to costs and risks. We will resolutely pursue the implementation of major strategic projects in each of our business lines and finalise our medium-term roadmap at Group level. We will move onto the next stage in the two major transformations common to all our business lines: integrating CSR objectives into the heart of both our activities and our culture of responsibility, and focusing on digital innovation to accelerate the use of new technologies for the benefit of our clients and to improve operational efficiency.

To deliver on this momentum, we can count on our Group’s entrepreneurial energy and capacity for collective action, which our teams show on a daily basis. Determined, committed and responsible, we put our corporate purpose into action: to build together, with our clients, a better and sustainable future.

We will move onto the next stage in the two major transformations common to all our business lines: integrating CSR objectives into the heart of both our activities and our culture of responsibility, and focusing on digital innovation to accelerate the use of new technologies for the benefit of our clients and to improve operational efficiency. -

1.1 HISTORY

On 4 May 1864, Napoleon III signed Societe Generale’s founding decree. Founded by a group of industrialists and financiers driven by the ideals of progress, the Bank’s mission has always been “to promote the development of trade and industry in France”.

Since its beginnings, Societe Generale has worked to modernise the economy, following the model of a diversified bank at the cutting edge of financial innovation. Its retail banking branch network grew rapidly throughout the French territory, increasing from 46 to 1,500 branches between 1870 and 1940. During the interwar period, the Bank became the leading French credit institution in terms of deposits.

At the same time, Societe Generale began to build its international reach by financing infrastructure essential to the economic development of a number of countries in Latin America, Europe and North Africa. This expansion was accompanied by the establishment of an international retail banking network. In 1871, the Bank opened its London branch. On the eve of World War I, Societe Generale was present in 14 countries, either directly or through one of its subsidiaries. The network was subsequently expanded by the opening of branches in New York, Buenos Aires, Abidjan and Dakar, and by acquiring stakes in financial institutions in Central Europe.

Societe Generale was nationalised by the French law of 2 December, 1945 and played an active role in financing the reconstruction of France. The Bank thrived during the prosperous post-war decades and contributed to the increased use of banking techniques by launching innovative products for businesses, including medium-term discountable credit and lease financing agreements, for which it held the position of market leader.

Societe Generale demonstrated its ability to adapt to a new environment by taking advantage of the banking reforms that followed the French Debré laws of 1966-1967. While continuing to support the businesses it partnered, the Group lost no time in focusing its business on individual clients. In this way, it supported the emergence of a consumer society by diversifying the credit and savings products it offered private households.

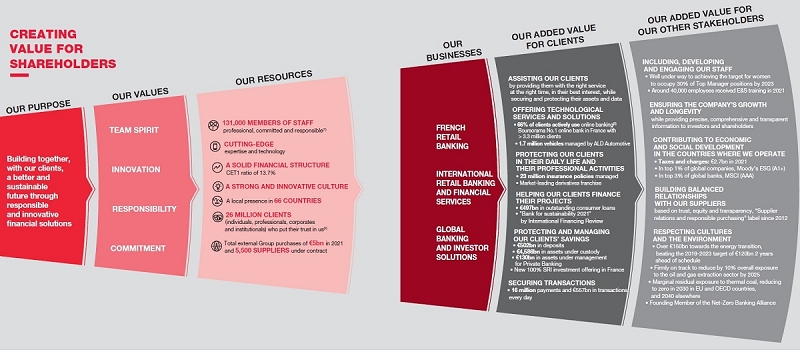

In June 1987, Societe Generale was privatised with a successful stock market launch and shares offered to Group staff. The Group developed a universal banking strategy, notably through its Corporate and Investment Banking arm, to support the worldwide development of its customers. In France, it expanded its networks by founding Fimatex in 1995, which later became Boursorama, now France’s leading online bank, and by acquiring Crédit du Nord in 1997. Internationally, it established itself in Central and Eastern Europe through Komerční Banka in the Czech Republic and BRD in Romania, and in Russia with Rosbank, while consolidating its growth in Africa in Morocco, Côte d’Ivoire and Cameroon, among other countries. The Group has more than 131,000 members of staff(1) active in 66 countries. It continues its process of transformation by adopting a sustainable growth strategy driven by its core values of team spirit, innovation, responsibility and commitment. Firmly focused on the future by helping our clients bring their projects to life, Societe Generale has embraced with conviction the opportunities of the digital age to best anticipate the needs of clients and staff members, and embody the bank of the 21st century. Drawing on more than 150 years of expertise at the service of its clients and the development of the real economy, in January 2020 Societe Generale group defined its purpose as “Building together, with our clients, a better and sustainable future through responsible and innovative financial solutions”.

-

1.2 PROFILE OF SOCIETE GENERALE

Societe Generale is one of the leading European financial services groups. Leveraging a diversified and integrated banking model, the Group combines financial strength and proven expertise in innovation with a strategy of sustainable growth, aiming to be the trusted partner for its clients, committed to the positive transformations of the world. Active in the real economy for over 150 years, with a solid position in Europe and connected to the rest of the world, Societe Generale employs over 131,000 members of staff(1) in 66 countries and supports on a daily basis 26 million individual clients, businesses and institutional investors(2) around the world. The Group offers a wide range of advisory services and tailored financial solutions to secure transactions, protect and manage assets and savings, and help its clients finance their projects. Societe Generale seeks to protect them in both their day-to-day life and their professional activities, offering the innovative services and solutions they require. The Group’s mission is to empower each and everyone who wants to make a positive impact on the future and defines its purpose as “Building together, with our clients, a better and sustainable future through responsible and innovative financial solutions”. (3)

(2)Excluding Insurance policyholders. The methodology used to count the number of clients in the International Retail Banking network changed in 2021. However, like-for-like, this has no impact on the change in the number of clients vs. 2020.

Societe Generale follows a strategy of responsible growth, fully integrating its CSR engagements and commitments to all its stakeholders: clients, staff, investors, suppliers, regulators, supervisors and representatives from civil society. The Group strives to respect the cultures and environment of all the countries where it operates.

■French Retail Banking, which encompasses the Societe Generale, Crédit du Nord and Boursorama brands. Each offers a full range of financial services with omnichannel products at the cutting edge of digital innovation;

■International Retail Banking, Insurance and Financial Services, with networks in Africa, Russia, Central and Eastern Europe and specialised businesses that are leaders in their markets;

■Global Banking and Investor Solutions, which offers recognised expertise, key international locations and integrated solutions.

The Group has an agile organisation based on 16 Business Units (business lines and regions) and 9 Service Units (support and control functions) to encourage innovation and synergies, and best meet the evolving requirements and behaviours of its clients. In a European banking sector undergoing radical industrial change, the Group is entering a new phase of its development and transformation.

Societe Generale is included in the principal socially responsible investment indices: DJSI Europe, FTSE4Good (Global and Europe), Bloomberg Gender Equality Index, Refinitiv Diversity and Inclusion Index, Euronext Vigeo (Europe and Eurozone), STOXX Global ESG Leaders indices and MSCI Low Carbon Leaders Index (World and Europe).

Results (In EURm)

2021

2020

2019

2018

2017

Net banking income

25,798

22,113

24,671

25,205

23,954

o.w. French Retail Banking

7,777

7,315

7,746

7,860

8,131

o.w. International Retail Banking and Financial Services

8,117

7,524

8,373

8,317

8,070

o.w. Global Banking and Investor Solutions

9,530

7,613

8,704

8,846

8,887

o.w. Corporate Centre

374

(339)

(152)

182

(1,134)

Gross operating income

8,208

5,399

6,944

7,274

6,116

Cost/income ratio(1)

68.2%

75.6%

71.9%

71.1%

74.3%

Operating income

7,508

2,093

5,666

6,269

4,767

Group net income

5,641

(258)

3,248

3,864

2,806

Equity (In EURbn)

Group shareholders’ equity

65.1

61.7

63.5

61.0

59.4

Total consolidated equity

70.9

67.0

68.6

65.8

64.0

ROE after tax

9.6%

-1.7%

5.0%

7.1%

4.9%

Total Capital Ratio(2)

18.7%

18.9%

18.3%

16.5%

17.0%

Loans and deposits (In EURbn)

Customer loans

458

410

400

389

374

Customer deposits

502

451

410

399

394

(1)Excluding the revaluation of own financial liabilities for 2017, before application of IFRS 9.

(2)Figures based on CRR2/CRD5 rules, excluding IFRS 9 phasing for 2021 and 2020.

Note: figures as published for the respective financial years. Definitions and potential adjustments presented in methodological notes on pages 41 to 46.

-

1.3 A STRATEGY OF PROFITABLE AND SUSTAINABLE DEVELOPMENT, BASED ON A DIVERSIFIED AND INTEGRATED BANKING MODEL

The Societe Generale Group has built a solid diversified banking model suited to the needs of its 26 million(1) corporate, institutional and individual clients. It is structured around three complementary and diversified businesses, all benefiting from strong market positions:

In the Retail Banking businesses, the Group focuses on development in European markets selected for their growth potential (France, Czech Republic and Romania) and Africa, where it has an historic presence, a refined understanding of the markets and top-tier positions. In International Financial Services, Societe Generale relies on franchises benefiting from leadership positions worldwide, notably in the operational vehicle leasing and fleet management businesses, and in equipment finance. In the Global Banking and Investor Solutions businesses, the Group provides high value-added solutions to its clients in the EMEA region, the US and Asia. Focused on Europe yet connected to the rest of the world, the Societe Generale Group capitalises on leadership positions driven by cross-business synergies to create value for stakeholders. The Group leverages its diversified model to meet the needs of its corporate and professional clients as well as its individual clients.

The rebound witnessed in the second half of 2020 continued throughout 2021, with all the Group’s businesses posting strong commercial and financial performances. As a result, the Group recorded its best results in history, enabling it to post strong profitability and offer shareholders an attractive dividend.

These financial performances reflect the Group’s efforts over recent years to strengthen the inherent quality of its businesses, improve operational efficiency, preserve the excellent robustness of the credit portfolio and manage its risks.

■merging its two banking networks in France (Vision 2025) to create a new bank serving nearly 10 million clients and and ramping up development of its online bank Boursorama following the announcement early in 2022 of the signing of a Memorandum of Understanding with ING with a view to offering the latter’s online banking clients the best alternative online banking solution;

■accelerating the growth of its long-term vehicle leasing business (ALD) with the announcement in early 2022 that ALD was to acquire LeasePlan. In the medium term, the Group’s plan is for the activities of this new vehicle leasing entity to become a third pillar, alongside retail banking and insurance, and corporate and investment banking.

The Group continued to pursue its selective resource allocation strategy and its focus on achieving the optimal region/offer/client mix for both itself and its clients, and confirmed its strong resolve to keep costs firmly in check. The adjustments that have been made are designed to mark out growing, high-margin businesses that enjoy strong commercial franchises.

■continued disciplined management of costs and scarce resources, combined with risk control, to contribute to the Bank’s solid balance sheet;

■digital transformation challenges, with the current crisis requiring it to step up efforts in this regard;

One of the Group’s priorities is to press on with its commercial development, focusing on quality of service, added value and innovation to deliver client satisfaction. Its goal is to become a trusted partner for its clients, making sound use of its digital capabilities to provide them with responsible and innovative financial solutions.

Organic growth will continue to be driven by unlocking internal synergies not only within each business but also between businesses. This will entail greater cooperation between Private Banking and the Retail Banking networks, cooperation along the entire Investor Services chain, cooperation between the Insurance business and the French and International Retail Banking networks, and cooperation between regions and Global Transaction Banking’s activities, among others.

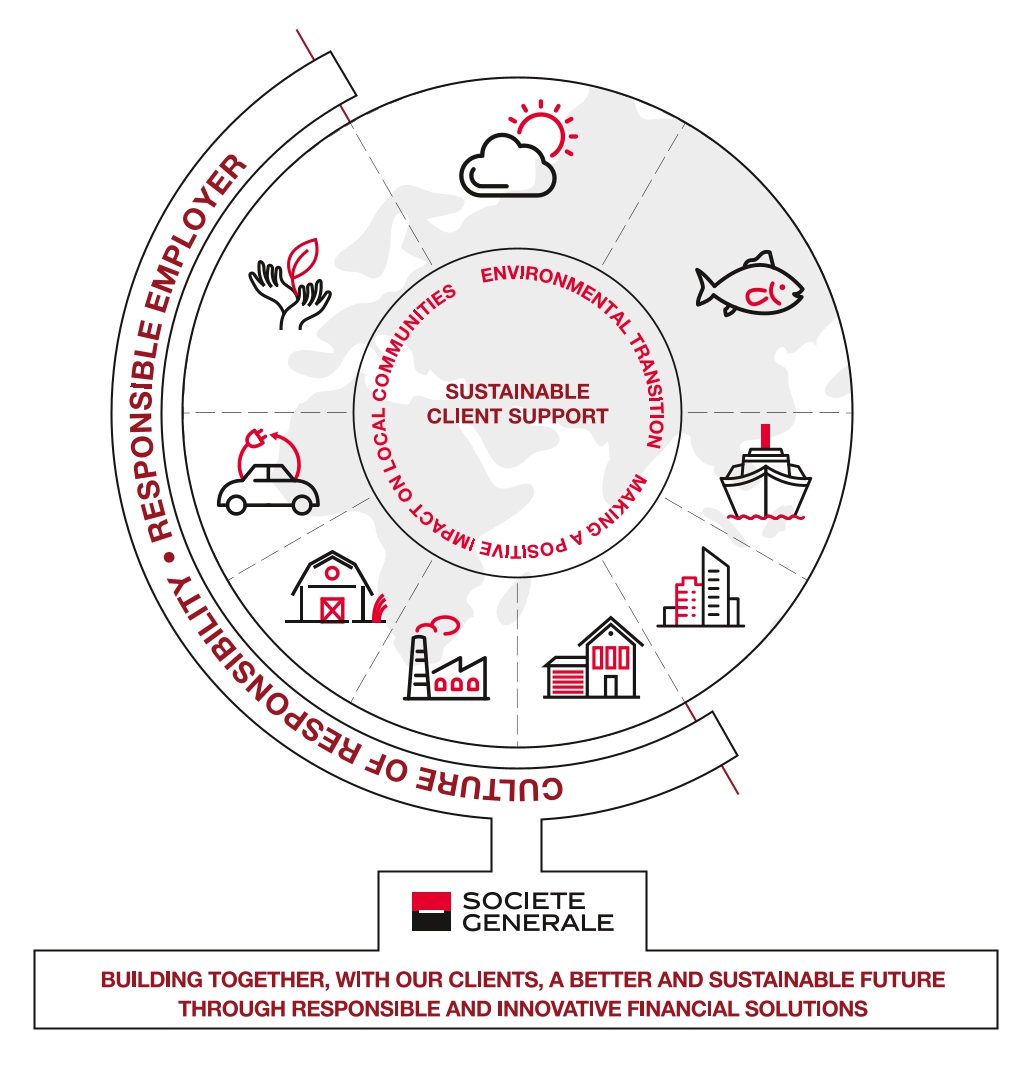

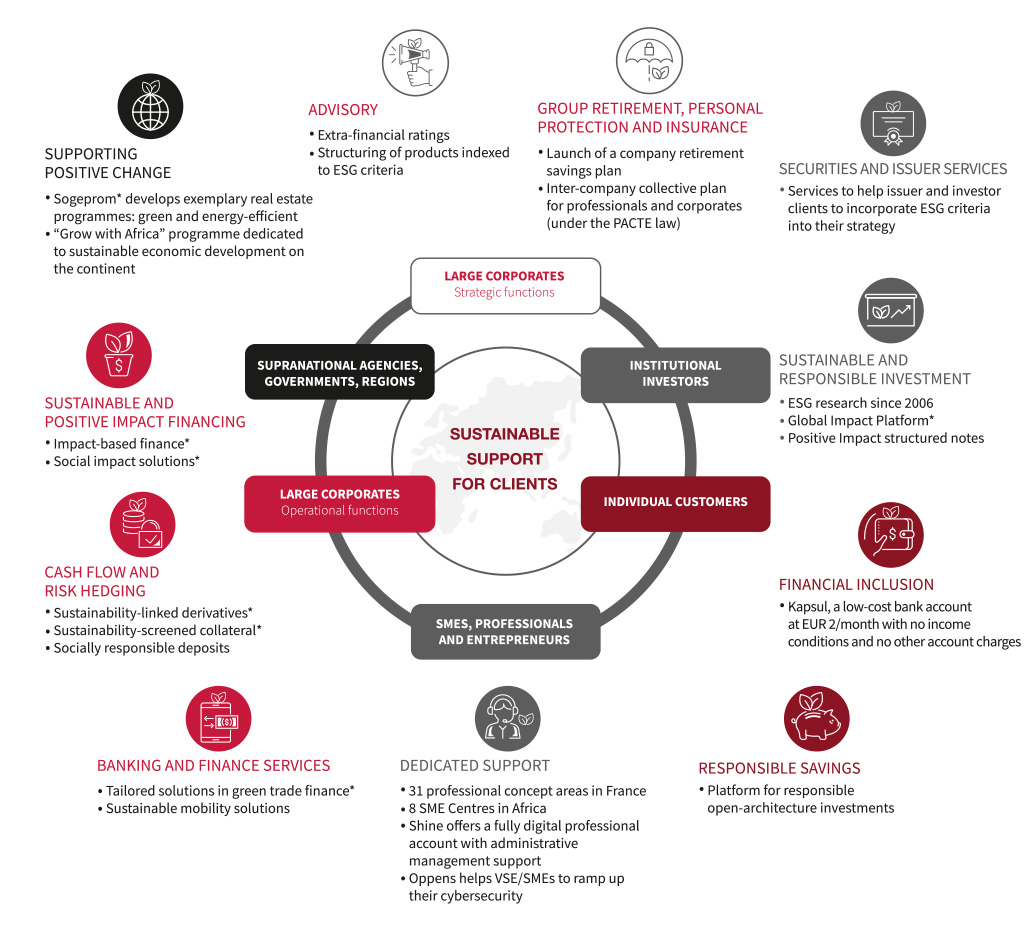

The Group has made certain changes to its Corporate Social Responsibility (CSR) governance. Since 1 January 2022, the Sustainable Development Department has reported directly to General Management, underscoring the Group’s decision to make CSR a core strategic concern. In keeping with its previous goals, Societe Generale has set its CSR targets for 2021 based on four development priorities, defined in light of the results from the materiality survey conducted at the end of 2020.

Two of these priorities involve being a responsible bank: fostering a culture of responsibility and being a responsible employer. The other two concern how the Group’s actions as a responsible bank can drive positive change: supporting the environmental transition and contributing to growth in local communities.

To guide its actions as a responsible bank, the Group has set itself the goal of embedding a culture of responsibility and applying the strictest control and compliance framework in the banking sector. It focuses on complying with all applicable ethics obligations and regulations, as well as with its own voluntary commitments, and on ensuring robust E&S risk management, channelling its efforts into specific actions to deliver a positive impact on the environment whilst remaining attentive to and working hand in hand with the various stakeholders in its global ecosystem.

For Societe Generale, being a responsible employer means providing a sound working environment and promoting diversity and professional development. This policy is key in boosting both employee engagement and overall performance. More specifically, the Group has identified five priority areas for action in human resources: Corporate Culture and Ethics Principles, Professions and Skills, Diversity and Inclusion, Performance and Compensation, and Occupational Health and Safety.

(1)Excluding the Group’s insurance companies. The methodology used to count the number of clients in the International Retail Banking network changed in 2021. However, like-for-like, this has no impact on the change in the number of clients vs. 2020.

The Group draws on its own exemplary conduct and exceptional resources to help its clients with their environmental transition and support sustainable local communities.

Conscious of the challenges its clients face when addressing global warming, Societe Generale has made the environmental transition a priority issue. Its goal is to be at the forefront of the energy transition. The core priorities of its climate change strategy, which has been approved by the Board of Directors, are as follows:

■develop a shared CSR culture in terms of risk management and commercial opportunities in connection with the energy transition;

■manage the climate impact of the Group’s activities (both its direct activities and those of its portfolios);

■support the Group’s clients in their energy transition, through a tailored product and service offering.

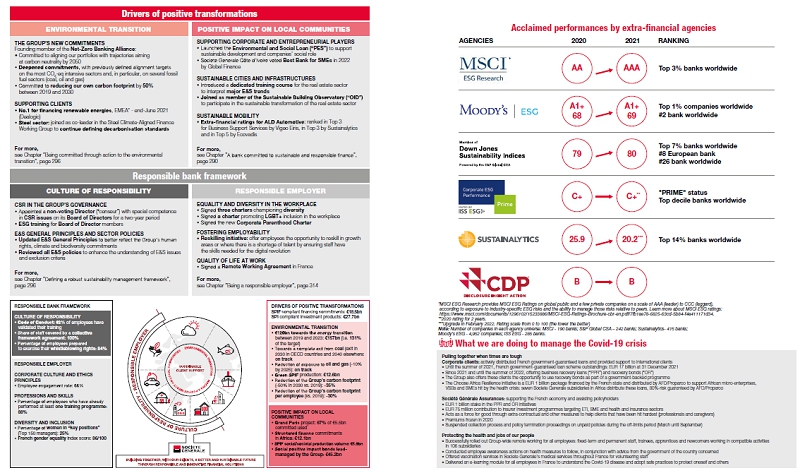

In response, the Group’s expertise in these areas has earned recognition from Dealogic, which ranked it No. 1 for financing renewable energies in EMEA at the end of June 2021. Societe Generale was also the recipient of one of the sector’s most prestigious awards when it was singled out as Best Bank in Sustainability in 2021 by International Financing Review (IFR).

Last, alongside its climate and environmental actions, Societe Generale also promotes sustainable regional development and strong local economies. It supports entrepreneurs, participates in projects to build sustainable cities and infrastructures and promotes clean mobility solutions in the regions in which it operates. Its actions in this respect are particularly noticeable in France, where they constitute one of the strategic objectives for the Group’s new retail banking network, and in Africa, through the Grow with Africa initiative.

Societe Generale’s efforts to achieve sustainable development have not gone unnoticed by the ratings agencies. Following on from its excellent ESG ratings in 2020, the Group again rated highly in 2021 across the board with all rating agencies in the three Environmental, Social and Governance segments, reflecting the depth of its commitment and the quality of its actions to promote sustainability.

The Group’s extra-financial ratings for the year were among the best in the banking sector: in the top 1% of all companies worldwide (out of 4,881 companies) in Moody’s ESG Solutions’ universe; in the top 3% banks worldwide (out of 190 banks) in MSCI’s universe; in the top quartile in the Sustainalytics universe out of a panel of 408 banks worldwide; and in the top 7% worldwide in the S&P Global Corporate Sustainability Assessment, placing the Group 8th in Europe and 26th worldwide out of 242 banks.

Societe Generale continues to foster a group-wide culture of responsibility and to strengthen its internal control framework, especially its Compliance operations, to meet the banking industry’s highest standards. It has also completed the rollout of its Culture and Conduct programme, embedding rules of conduct and strong shared values throughout the entire company.

Societe Generale announced in 2021 the end of two separate legal proceedings brought by the US Departmentof Justice, one relating to Societe Generale’s IBOR submissions and certain transactions involving Libyan counterparties, and the other relating to US economic sanctions compliance. In requesting the courts to dismiss the legal proceedings, the DOJ confirmed that the Bank had fully complied with its obligations under the related deferred prosecution agreements (DPA).

Last, the Group is determined to press ahead with its stringent and disciplined approach to risk management - maintaining credit portfolio quality, continuing efforts regarding operational risk control and compliance - and to its capital allocation management.

In line with its strategy to fully address its clients’ needs and in consideration of the new, more demanding regulatory environment, the Group’s focus will remain on optimising its consumption of scarce capital and liquidity resources and maintaining a highly disciplined approach to costs and risk management.

In 2022, the Group intends to build on the commercial momentum already embedded in its businesses and strengthen the resilience of its financial performance amid a more uncertain environment.

Excluding the Single Resolution Fund contribution, the underlying cost to income ratio is expected to range between 66% and 68% in 2022, and improve thereafter thanks to the cost reductions initiatives announced in 2021.

The cost of risk is expected to be below 30 basis points in 2022, i.e. slightly higher than the 2021 level. In the wake of recent developments in Ukraine and Russia, the Group announced on 3 March that it was not changing its cost of risk target and would update it, if necessary, at the time of its Q1 22 results publication.

The Group is aiming for a CET1 ratio at least between 200-250 basis points above the regulatory requirement, including after the entry into force of the regulation finalising the Basel III framework.

The Board of Directors approved an attractive shareholder distribution of the 2021 financial results equivalent to EUR 2.75 per share. A cash dividend of EUR 1.65 per share will be proposed to the General Meeting of Shareholders on 17 May 2022.

The Group is also envisaging a share buyback programme of approximately EUR 915 million, i.e. equivalent to EUR 1.10 per share. It has been decided to exceptionally split the pay-out as 60% in cash and 40% through a share buy-back. In future, the Group intends to maintain a dividend policy based on a 50% pay-out ratio of underlying Group net income with up to 20% of the pay-out in the form of a share buyback.

The French Retail Banking business has made sweeping changes to its model, in particular on the back of rapid changes in client behaviours and demand for ever-increasing convenience, expertise and customised products and services. The pace of transformation accelerated in 2020, with two major strategic initiatives: the planned merger of Crédit du Nord and Societe Generale, and moves to ramp up growth at Boursorama. These initiatives are designed to cement the Group’s winning combination of a fully online banking model coupled with a network banking model offering both digital and human expertise – a combination that stands out in the French market. Over the course of 2021, the Group successfully moved ahead with the first stages of its merger project, the key principles of which are as follows:

■a new model based on a full merger of the Crédit du Nord and Societe Generale retail banks, combining the strengths of each within a single bank: one branch network, one head office and one IT system, with nearly 10 million clients served by 25,000 employees in 2025;

■a bank with local roots comprising 11 regional divisions with broader responsibilities, nationwide coverage through 1,450 branches to ensure continued branch presence, and a new branding approach that reflects these regional roots;

■a bank that is more responsive, accessible and efficient, with a remodelled organisation to improve client experience and operational efficiency;

■a bank better adapted to the specific needs of each client category, with the aim of ranking among the top banks for client satisfaction by training its bankers to a high standard and offering a quality client experience, whether in a branch, over the telephone or online;

■a responsible bank that steps up its ESG commitments to enhance our positive local impact and confirming our commitment to being a responsible employer by supporting employees throughout the merger, and making no compulsory layoffs.

The ambition is to rank among the leaders for client satisfaction for our core client base and to create a banking model that increases profitability and conforms to the most stringent standards of responsibility. From a financial perspective, the merger will unlock considerable cost synergies, with a net cost-base reduction target of more than EUR 350 million by 2024 and around EUR 450 million by 2025, compared with 2019. The cost of the tie-up has been estimated at between EUR 700 million and EUR 800 million. The return on normative equity under Basel III is expected to range between 11% and 11.5% in 2025, equating to more than 10% under Basel IV.

■maximising the potential of the integrated bancassurance model by anticipating changes in the life-insurance market and taking advantage of strong client take-up potential for personal protection and non-life insurance;

■increasing business among corporate and professional clients by providing strategic advisory services and comprehensive solutions;

■leveraging the expertise available in Private Banking to satisfy the expectations of high net worth clients in the French networks.

In Asset & Wealth Management and Private Banking, the disposal of Lyxor to Amundi forms part of Societe Generale’s strategy of operating in open architecture, distributing savings solutions to clients across both of its networks. By offering its clients investment and asset management solutions through partnerships with external asset managers, Societe Generale gives its savers access to the best investment expertise in France and internationally, while at the same time responding to their growing demand for socially responsible investment. The new Wealth & Investment Solutions Division within Private Banking focuses on structuring savings, asset management and investment solutions for the Group’s private banking and retail banking networks, as well as structured asset management solutions for its Global Markets clients.

Last, the Group continues to support the development of its online bank Boursorama, which has consolidated its leadership position in France with a bumper year in terms of client acquisition: more than 800,000 new clients in 2021, bringing their total number to 3.3 million. Over the next few years, Boursorama intends to press ahead with investments to win over new clients and is targeting more than 4 million clients by the end of 2022, one year ahead of schedule. Societe Generale also announced that Boursorama had signed a Memorandum of Understanding with ING with a view to offering its online banking clients in France the best possible alternative banking solution that furnishes dedicated client experience and support features. The two banks intend to sign a definitive agreement by the end of April 2022. The Group has confirmed its aim of taking Boursorama to maturity, targeting 4.5 million clients and a return on normative equity of more than 25% by 2025.

International Retail Banking and Financial Services is a profitable growth driver for the Group thanks to its leading positions in high-potential markets, its operational efficiency and digital transformation initiatives, and its ability to unlock synergies with other Group activities. These businesses have undergone a major transformation over the last few years to fully refocus the portfolio, introduce a more optimised model and improve the underlying risk profile.

International Retail Banking activities are mainly located outside the Eurozone and benefit from positive long-term growth fundamentals, although the Covid-19 pandemic and associated economic crisis have somewhat slowed their historical trajectory of continuous growth. The Group nevertheless plans to press on with its strategy of consolidating leadership positions and pursuing responsible growth within its international banking activities in Europe and Africa. Its capacity to meet its clients’ needs, coupled with its innovative, unique and efficient platforms, will serve it well in this undertaking:

■in Europe, the health crisis has sharply accentuated underlying trends, confirming the strategic vision of the Group’s target retail banking model, as well as the relevance of the transformation plans undertaken, which place special emphasis on ramping up digital transformation. Accordingly, the Group intends to put the finishing touches to its omnichannel banking model in the Czech Republic with its KB Change 2025 strategic plan, consolidate its franchise’s position in Romania as one of the country’s three leading banks. The Group’s exposure to Russia is limited - less than 2% of its overall exposure - and the Group is closely monitoring events in the region’s geopolitical situation. The Group also intends to tap into the full potential of its consumer finance activities in Europe through both its own retail banking networks and its specialist subsidiaries in and outside France

■in Africa, the Group plans to take advantage of the continent’s strong potential for economic growth and bank account penetration by building on its position as one of the three international banks with the largest footprint in Africa, where it enjoys leading positions in the Mediterranean Basin, as well as in Côte d’Ivoire, Guinea, Cameroon and Senegal.

As part of the Grow with Africa programme developed in partnership with a panel of international and local partners, Societe Generale has announced several sustainable growth initiatives to foster positive transformation across the continent. Accordingly, the Group is concentrating on providing multidimensional support to African SMEs, funding infrastructure, supporting the energy transition and developing innovative financing solutions.

Financial Services and Insurance enjoy competitive positions and strong profitability, in particular with ALD and Insurance, both of which have robust growth potential. These are the businesses that best withstood the economic shock of 2020. Incidentally, they are continuing to roll out their programmes to innovate and transform their operational model.

■In Insurance, the Group plans to accelerate the rollout of its bancassurance model across all retail banking markets and all segments (life insurance, personal protection and non-life insurance), as well as of its digital strategy. The aim is to enhance its product range and client experience within an integrated omnichannel framework, while diversifying its business models and growth drivers through a strategy of innovation and partnerships. This growth strategy goes hand in hand with greater commitments to responsible finance at SG Assurances.

■In Operational Vehicle Leasing and Fleet Management, the Group sees the planned acquisition of LeasePlan as an opportunity to create a global leader in sustainable mobility solutions. The new entity is poised to be No. 1 worldwide, excluding captives and financial leasing companies. With a total fleet of 3.5 million vehicles at end-December 2021 and operations in over 40 countries, it boasts highly complementary expertise and prospective synergies. The Group also intends to develop new activities and services in a mobility sector undergoing radical change. Having boosted its investment capacities and unique know-how, ALD has positioned itself at the heart of this changing world of mobility, asserting its global leadership to become a fully integrated player in sustainable mobility solutions with the rollout of its Move 2025 strategic plan and the planned acquisition of LeasePlan. It is now particularly well placed to take full advantage of the market’s strong growth. To this end, ALD forged ahead with its active innovation and digitalised strategy over the year.

■Last, for Vendor and Equipment Finance, the Group plans to build on its leadership position in Europe in those top-tier markets to increase revenue and improve profitability. It plans to draw on its service quality, capacity for innovation, product expertise and dedicated teams to retain its preferred partner status with vendors and clients alike.

Societe Generale also plans to continue moving forward with its strategy of unlocking synergies between the activities of the various businesses in this division and elsewhere within the Group, with Private Banking and the regional Corporate and Investment Banking platforms, by developing its commercial banking services such as trade finance, cash management, payment services and factoring, and by pursuing the development of its bancassurance model.

Global Banking and Investor Solutions stands on broad and diversified foundations: it has built up a solid and stable diversified client base and benefits from high value-added product franchises and recognised sector expertise backed by a global network. It serves the financing and investment needs of a broad and diversified client base spanning corporates, financial institutions and public-sector entities. Having undergone a considerable transformation in recent years - reducing its breakeven point and de-risking the Global Markets business, and adjusting the size of its businesses - GBIS is focused on delivering value to all its stakeholders through sustainable and profitable growth.

Its growth strategy is consistent with the position of current economic growth opportunities, i.e. in increased financing needs for infrastructure and the energy transition, greater investment in private debt and the growing demand for investment solutions. At the same time, it is gradually and coherently adjusting the size of its businesses, particularly between Global Markets and Investor Services and Financing and Advisory, making targeted capital allocations to identified growth initiatives for particular client segments, businesses and regions.

The Group has also made it a priority to develop “ESG by design” businesses, setting itself the target of doubling ESG-related revenues by 2025 in both Global Markets and Investor Services and Financing and Advisory.

■reducing costs to improve operating leverage without business attrition and in keeping with its long-term commitment to disciplined cost control;

■adopting stringent management of both market and credit risks, notably against a backdrop of weaker market risk appetite, and prudent management of its counterparty risk, aiming to maintain a healthy diversification of all risk categories across its businesses.

RECENT DEVELOPMENTS AND OUTLOOK

The latest wave of the epidemic has incurred a proportionally lower death toll compared to the very high contamination levels. The economy’s greater adaptability has mitigated the impact on business, but the withdrawal of temporary support measures is only partly being offset by the economic reopening and recovery support measures.

Prevailing uncertainty over events in Ukraine and Russia is making it difficult to forecast the impact on the global economy and the Group, and has furthermore sparked a return of volatility in financial markets. We expect energy prices (notably oil and gas) to remain high in 2022 on back of supply chain disruptions and the consequences of the situation in Ukraine. These factors are likely to contribute to a slowdown in eurozone growth during 2022 and 2023.

Tensions in the job market are playing out in wage adjustments and specifically a rise in the minimum wage. We forecast that these gains, combined with rising energy prices, may trigger short-term inflation spikes in Europe and the US. Further out, new monetary policy strategies on both sides of the Atlantic should drive inflation closer to target, contrary to the past decade during which inflation undershot central bank targets.

The US Federal Reserve (Fed) could tighten its monetary policy in light of the increased risk of heightened inflation expectations and a wage-price spiral taking hold in the US. Emerging markets are expected to continue the monetary tightening started in early 2021, while China has already begun its measured easing cycle. Low to negative real interest rates should help trigger a global deleveraging process. That said, uncertainties persist over market expectations as consensus on the ability of central banks to keep inflation under control could shift suddenly and lead to sharper tightening of financial conditions. The 2021 regulatory landscape was marked by stimulus and easing measures in line with those of 2020 to enable banks to support the economy. Some of these measures will continue in 2022. Governments have lent massive support to the financing of companies. In France, support measures were implemented by way of government-backed loan schemes totalling EUR 14.3 billion at end-December 2021, and recovery loans.

These measures will most likely be maintained or even strengthened in 2022 in light of the continued health crisis and against the backdrop of the French elections.

The European Commission (EC), the European Central Bank (ECB) in its capacity as prudential supervisor, the European Banking Authority (EBA) and the High Council for Financial Stability (HCSF) have used the flexibility of prudential regulations to act on the liquidity and solvency of banks. These regulatory adjustments included:

■the easing of countercyclical capital buffer requirements with the possibility of using them subject to automatic remedial action (maximum distributable amount mechanism and submission of a capital conservation plan);

■greater flexibility in applying the criteria for downgrading moratoria and a recommendation that the pro-cyclical impacts of IFRS9 application be supervised.

The trend is now towards normalisation. The ECB decided not to extend its recommendation on dividend pay-outs and share buybacks beyond 30 September 2021. This recommendation involved limiting divident payment and share buyback amounts for all banks under its direct supervision. Last, the flexibility measure taken by the ECB to allow banks to have a Liquidity Coverage Ratio (LCR) below the regulatory threshold of 100% ended on 31 December 2021.

Beyond the prevailing economic conditions, several structural regulatory projects aim to strengthen the prudential framework, support environmental and digital transitions, protect consumers and develop European capital markets.

The year 2021 put the spotlight back on finalising the implementation of the Basel III prudential agreements in the European Union. In October 2021, the European Commission published its new banking rules - the proposed CRR3 regulation and the CRD6 directive - which will enter into force on 1 January 2025. The timetable for rolling out the reforms in the main non-EU jurisdictions remains uncertain and is not expected to coincide with the Basel timetable of 1 January 2023.

In accordance with the European Green Deal proposed by the European Commission in December 2019, environmental and sustainability issues took centre stage in 2021. The financial sector is facing highly ambitious expectations, the aim being to rapidly mobilise capital flows to achieve carbon neutrality and lay the groundwork for a sustainable economy. Work on the EU taxonomy for sustainable activities is ongoing; activities are classified as “sustainable”, “harmful” or “social”. Accordingly, banks and large companies are poised to publish their first climate reports in 2022.

Banks are expected to better integrate their climate risk exposure when managing risks and be more transparent about disclosing ESG risks in their prudential publications. The ECB will organise climate stress testing on top of climate pilot exercises run by the French Prudential Supervision and Resolution Authority (Autorité de contrôle prudentiel et de résolution - ACPR) and the European Banking Authority (EBA). Debate is intensifying over the prudential treatment of assets that are harmful to the climate and will be the topic of an EBA report in 2023. The European Union was a trailblazer for ESG-related topics, so the issue of harmonising European standards with those introduced in other jurisdictions will be a key consideration in 2022.

■the Digital Operations Resilience Act (DORA) to strengthen cybersecurity and the monitoring of outsourced services;

The year 2021 was also marked by in-depth work on significant topics related to payments, i.e. the EPI project and ECB’s study of a central bank digital currency (CBDC) and of an acceleration in the spread of instant payments. These projects will continue in 2022 and should be supplemented by Open Finance proposals for which the DSP2 Directive assessment will be an important step.

In order to finance these environmental and digital transitions, regulated savings may be reformed with the introduction of national and European financial regulations fostering the redirecting of these savings.

Consumer issues is also set to attract considerable attention in both France and Europe. In particular, plans to revise MiFID, PRIIPS and consumer credit directives are under way at European level. Many issues related to the pricing and transparency of banking products are also being debated at the national level: protection for the self-employed (pricing, assets, financing) will continue to take centre stage, and developments in insolvency procedures and the regulation of securities will affect the mechanisms at work in the financing of the economy for the smallest businesses.

Last, in a post-Brexit environment and as part of developing its strategic autonomy plan announced in January 2021, the European Commission gave new momentum to the development of the Capital Markets Union (CMU).

At the end of 2021, the Commission proposed practical steps towards a real CMU following the European action plan published in 2020 with (i) the publication of legislative proposals for the revision of MIFIR, (ii) the publication of the directive relating to alternative management and that of the regulation on long-term investment funds, and (iii) the establishment of a European single access point (ESAP) for financial and non-financial information publicly disclosed by companies.

At the same time, the Commission launched a targeted consultation to possibly amend the Listing Act, with the aim of ensuring the attractiveness of capital markets for EU companies and facilitating access to capital for small and medium-sized enterprises.

-

1.4 THE GROUP’S CORE BUSINESSES

French Retail Banking

International Retail Banking

and Financial Services

Global Banking

and Investor Solutions

2021

2020

2019

2021

2020

2019

2021

2020

2019

Number of employees (in thousands)(1)

33.8

34.3

35.3

57.4

59.3

62.8

19.4

20.2

21.3

Number of branches(2)

1,849

2,068

2,375

2,038

2,156

2,409

n/s

n/s

n/s

Net banking income (in EURm)

7,777

7,315

7,746

8,117

7,524

8,373

9,530

7,613

8,704

Group net income (in EURm)

1,492

666

1,131

2,082

1,304

1,955

2,076

57

958

Gross loan book outstandings(3)(in EURbn)

238.8

217.6

201.1

145.3

135.5

138.2

193.5

154.7

158.1

Net loan book outstandings(4)(in EURbn)

234.7

212.8

196.2

139.8

130.1

111.3

192.1

153.1

157.1

Segment assets(5) (in EURbn)

262.5

256.2

232.8

358.5

331.9

333.7

692

707.8

674.4

Average allocated capital (regulatory)(6) (in EURm)

11,149

11,427

11,263

10,246

10,499

11,075

14,916

14,302

15,201

(1)Headcount at end of period excluding temporary staff.

(2)Number of main branches for French Retail Banking

(2)Customer loans, deposits and loans due from banks, lease financing and similar agreements and operating leases. Excluding repurchase agreements. Excluding entities that are reclassified under IFRS 5.

(3)Loan book outstandings net of impairments.

(4)Segment assets included in Note 8.1 of the Consolidated Financial Statements (segment reporting). 2020 amounts restated (See Note 1.7 of the Consolidated Financial Statements.

(5)Average allocated capital calculated on 11% of risk-weighted assets.

1.4.1 FRENCH RETAIL BANKING

French Retail Banking offers a wide range of products and services suited to the needs of a diversified base of individual and professional clients, businesses, non-profit associations and local authorities.

Leveraging the expertise of its teams and an efficient multi-channel distribution system, the pooling of best practices, and the optimised and digitalisation of processes, French Retail Banking combines the strengths of three complementary brands: Societe Generale, the renowned national bank, Crédit du Nord, a group of regional banks, and Boursorama Banque, a major online bank.

The Retail Banking networks are innovating to build the relationship-focused banking group of tomorrow. French Retail Banking is exemplified by its:

On 7 December 2020, the Societe Generale Group announced the launch of merger plans for the Societe Generale and Crédit du Nord banking networks and for Boursorama to enter a new phase of maturity, with a goal of 4.5 million clients by 2025.

French Retail Banking strives to improve client satisfaction across all segments and to further develop value-added services and assist businesses with their expansion in France and worldwide. It capitalises on synergies with the specialised business lines, notably with Insurance, Private Banking, and Corporate and Investment Banking. For example, French Retail Banking markets insurance products developed by Sogécap and Sogessur, subsidiaries operating in the International Retail Banking and Financial Services Division.

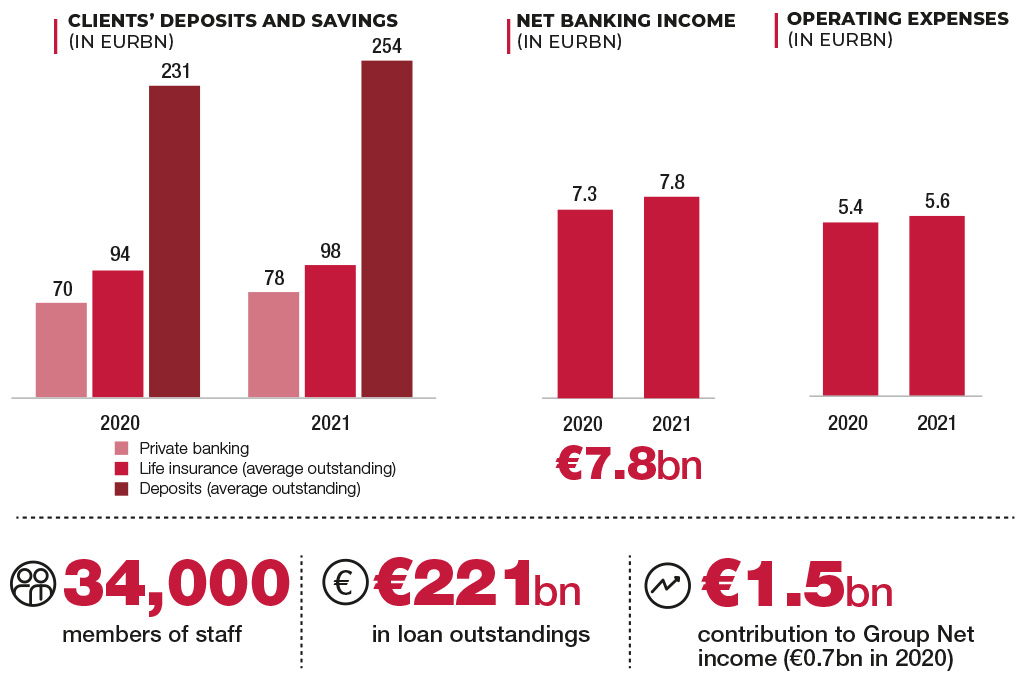

Life insurance outstandings amounted to EUR 98 billion at the end of 2021, compared with EUR 93.6 billion in 2020.

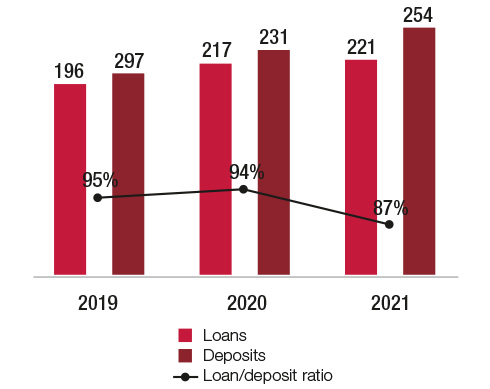

The networks continue to support the economy and help clients finance their projects, with growth in average loan outstandings up from EUR 217 billion in 2020 to EUR 221 billion in 2021. At the same time, and amid rife competition, deposit inflows showed resilience and resulted in a loan-to-deposit ratio of 86.8% in 2021, down 7 points on 2020.

The Societe Generale network offers solutions tailored to the needs of its 6.7 million individual clients as well as almost 430,000 professional clients, non-profit associations and corporate clients, representing EUR 108 billion in outstanding deposits and EUR 84 billion in outstanding loans in 2021.

■approximately 1,202 main branches located mainly in urban areas where a large proportion of national wealth is concentrated;

■an exhaustive and diversified range of products and services, ranging from savings vehicles and asset management solutions to corporate finance and payment means;

■a comprehensive and innovative omnichannel system spanning Internet, mobile, telephone and service platforms.

Societe Generale continued to expand its network and increase its service offering in 2021 in response to its clients’ requirements and with a view to enhancing customer satisfaction. It notably improved its digital offering, focusing especially on professional and corporate clients - introducing a revamped the app and websites, promoting electronic signature services and other advantages - added Corporate and Investment Banking’s SME/mid-cap services to the range of expertise available to corporate clients, and developed Shine, its 100% online banking subsidiary for professionals and VSBs. It also announced plans to look into the option of sharing ATMs with Crédit du Nord, BNP Paribas and Crédit Mutuel, with a view to improving accessibility for the clients of all four banks.

Societe Generale has made sustainable development the linchpin of its strategy. It took further steps last year to limit its direct environmental impact by reducing waste and shrinking its carbon footprint, and to address social issues. It also developed a new range of services designed to help clients achieve their own sustainable development and energy transition goals: 2021 saw the introduction of social and environmental loans for corporates, as well as a new range of 100% SRI savings vehicles for individual clients.

In 2021, Societe Generale and Crédit du Nord confirmed plans to merge, combining their two networks to form a new retail bank serving 10 million clients. Four key principles have been defined for this new entity: it will be a bank with local roots, a bank that is more responsive, accessible and efficient, a bank better adapted to the specific needs of each client category, and a bank that is responsible. The two networks will officially merge on 1 January 2023, with a progressive rollout of the new organisation culminating in 2025.

The Crédit du Nord group consists of nine regional banks – Courtois, Kolb, Laydernier, Nuger, Rhône-Alpes, Société Marseillaise de Crédit, Tarneaud, Société de Banque Monaco and Crédit du Nord – and an investment services provider, the brokerage firm Gilbert Dupont.

Crédit du Nord entities are characterised by a large degree of autonomy in managing their activities, which is chiefly expressed by rapid decision-making and responsiveness to client demands.

The quality and strength of the results of the Crédit du Nord group have been recognised by the market and are confirmed by the long-term A- rating attributed by Fitch.

Crédit du Nord serves 1.8 million individual clients(1), 213,000 professional clients and non-profit associations and 47,000 corporate and institutional clients. In 2021, its average outstanding deposits totalled EUR 57 billion, compared with EUR 52 billion in 2020, while average loan outstandings stood at EUR 52 billion, compared with EUR 50 billion in 2020.

Boursorama is a subsidiary of Societe Generale and a pioneer and leader in France for its three main businesses: online banking, online brokerage and online financial information at boursorama.com, ranked No. 1 for economic and stock market news. An online bank accessible to all, without any revenue or financial wealth prerequisites, Boursorama’s promise is the same as it was when it was first created, i.e. simplify clients’ lives at the most competitive price and furnish the best service possible in order to boost their purchasing power.

Boursorama currently serves over 3.3 million clients – a figure it has quadrupled in the last five years. This rapid growth has been matched by an increase in the bank’s outstandings (in excess of EUR 48 billion at end-December 2021), demonstrating the appeal of its fully online model based on client autonomy and a comprehensive range of banking products and services with automated processes.

In 2021, Boursorama extended its range, particularly as regards investment solutions (such as its MATLA retirement savings plan: a 100% SRI solution and the least expensive on the market) and life insurance and brokerage products (its new PrimeTime offer gives clients access to Accelerated Book Building (ABB) transactions through the PrimaryBid platform). It also launched a warranty extension insurance and made changes to its Freedom package for 12-17 year olds.

As in 2020, Boursorama was acclaimed the least expensive bank for the 14th consecutive year at the Customer Relationship Podium Awards in 2021, taking 6th position all sectors included. It continues to boast an excellent recommendation rate of 86%, coupled with a Net Promoter Score of +40. Buoyed by these results, it is confident of achieving its targets of more than 4 million clients by 2023 and profitability of over 25% by 2025.

-

2.2 GROUP ACTIVITY AND RESULTS

Information followed by an asterisk (*) is indicated as adjusted for changes in Group structure and at constant exchange rates.

(In EURm)

2021

2020

Change

Net banking income

25,798

22,113

16.7%

17.7%*

Operating expenses

(17,590)

(16,714)

+5.2%

+5.8%*

Gross operating income

8,208

5,399

52.0%

55.1%*

Net cost of risk

700

(3,306)

-78.8%

-78.6%*

Operating income

7,508

2,093

x 3.6

x 3.7*

Net income from companies accounted for by the equity method

6

3

100%

100%*

Net profits or losses from other assets

635

(12)

n/s

n/s

Impairment losses on goodwill

(114)

(684)

83.3%

83.3%*

Income tax

(1,697)

(1,204)

41.0%

43.2%*

Net income

6,338

196

x 32.3

x 43.8*

o.w. noncontrolling interests

697

454

53.5%

53.6%*

Group net income

5,641

(258)

n/s

n/s

Cost-to-income ratio

68.2%

75.6%

Average allocated capital(1)

52,634

52,091

ROTE

11.7%

-0.4%

(1)Amounts restated compared with the financial statements published in 2020 (See Note1.7 of the financial statements).

Net banking income was substantially higher in 2021, up +16.7% (+17.7%*) vs. 2020, and +16.1% (+17.2%*) vs. 2020 on an underlying basis, with a very strong momentum in all businesses.

French Retail Banking posted a solid performance in 2021. As a result, net banking income (excluding PEL/CEL provision) increased by +4.8% vs. 2020, driven by the recovery in net interest income and by buoyant fee income, particularly in respect of financial fees.

International Retail Banking & Financial Services enjoyed strong revenue growth (+9.9%* vs. 2020), underpinned by the excellent momentum in Financial Services (+32.0%* vs. 2020) and Insurance (+8.6%* vs. 2020). International Retail Banking benefited from a rebound in its activities (+2.8%* vs. 2020).

Global Banking & Investor Solutions delivered a remarkable performance, with revenues up +25.2% (+26.1%*) vs. 2020. Financing & Advisory posted a record performance, with growth of +14.8% (+15.8%*) vs. 2020, while Global Markets & Investor Services posted substantially higher revenues than in 2020, up +35.6% (+36.9%*).

In 2021, operating expenses totalled EUR 17,590 million on a reported basis and EUR 17,211 million on an underlying basis (adjusted for transformation costs), i.e. an increase of +4.3% vs. 2020.

The increase can be explained primarily by the rise in variable costs associated with revenue growth (EUR +701 million) and the increase in the contribution to the Single Resolution Fund (EUR +116 million). The other operating expenses declined by EUR 70 million, excluding structure effect.

Driven by a very positive jaws effect, underlying gross operating income grew substantially (+51.0%) to EUR 8,470 million and the underlying cost to income ratio improved by nearly 8 points (67.0% vs. 74.6% in 2020).

Excluding the contribution to the Single Resolution Fund (SFR), the underlying cost to income ratio is expected to be between 66% and 68% in 2022 and improve thereafter. This aggregate, excluding the contribution to the SRF, amounts to 64.7% in 2021, bearing in mind that SFR contribution totalled EUR 586 million in 2021.

The radical transformations that were announced for the Group in 2021 have led to changes in the 2023 cost outlook. The various initiatives in progress will help push down the Group’s underlying cost-to-income ratio beyond 2022, excluding the Single Resolution Fund contribution year after year.

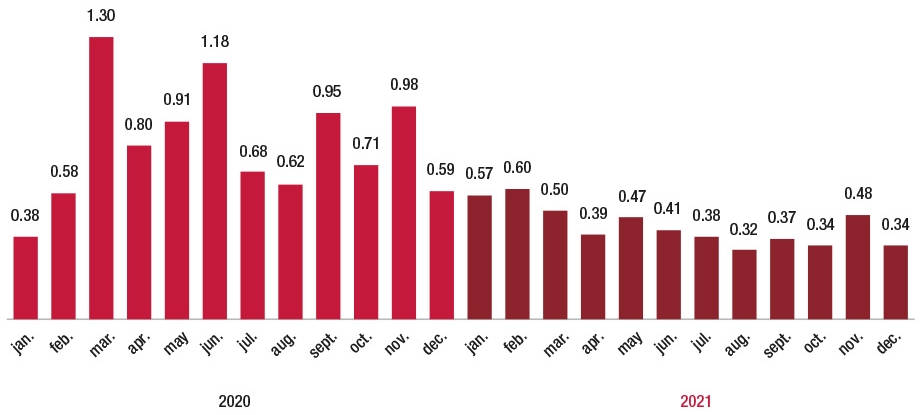

In 2021, the cost of risk declined to a low 13 basis points, which was lower than the 2020 level of 64 basis points, i.e. EUR 700 million (vs. EUR 3,306 million in 2020). The amount breaks down to a provision on non-performing loans of EUR 949 million and a provision write-back on performing loans of EUR 249 million.

The Group granted government-guaranteed loans (“PGE”) to support its clients during the crisis. At 31 December 2021, the residual amount of government-guaranteed loans represented around EUR 17 billion. In France, this loan category totalled approximately EUR 14 billion, while net exposure stood at around EUR 1.5 billion.

The doubtful loan ratio stood at 2.9% at 31 December 2021, a decline on the end-September 2021 level of 3.1%. The gross coverage ratio on doubtful loans for the Group was 51% at 31 December 2021.

Book operating income totalled EUR 7,508 million in 2021 compared with EUR 2,093 million in 2020. Underlying operating income came to EUR 7,770 million compared with EUR 2,323 million in 2019.

Net profits or losses from other assets totalled EUR 635 million in 2021, of which EUR 439 million from the disposal of Lyxor’s asset management activities and EUR 185 million in capital gains from the disposal of real estate.

On back of the review of International Retail Banking’s financial trajectory, the Group recorded an impairment loss on goodwill of EUR 114 million in 2021 relating to the acquisition of the CGU Africa, Mediterreanean Basis and Overseas.

-

2.3 ACTIVITY AND RESULTS OF THE CORE BUSINESSES

2.3.1 RESULTS BY CORE BUSINESSES

French Retail

Banking

International

Retail Banking

and Financial

Services

Global Banking

and Investor

Solutions

Corporate

Centre

Group

(In EURm)

2021

2020

2021

2020

2021

2020

2021

2020

2021

2020

Net banking income

7,777

7,315

8,117

7,524

9,530

7,613

374

(339)

25,798

22,113

Operating expenses

(5,635)

(5,418)

(4,203)

(4,142)

(6,863)

(6,713)

(889)

(441)

(17,590)

(16,714)

Gross operating income

2,142

1,897

3,914

3,382

2,667

900

(515)

(780)

8,208

5,399

Net cost of risk

(104)

(1,097)

(504)

(1,265)

(86)

(922)

(6)

(22)

(700)

(3,306)

Operating income

2,038

800

3,410

2,117

2,581

(22)

(521)

(802)

7,508

2,093

Net income from companies accounted for by the equity method

1

(1)

0

0

4

4

1

0

6

3

Net profits or losses from other assets

24

158

18

15

(10)

0

603

(185)

635

(12)

Impairment losses on goodwill

-

-

-

-

-

-

(114)

(684)

(114)

(684)

Income tax

(575)

(291)

(840)

(531)

(469)

100

187

(482)

(1,697)

(1,204)

Net income

1,488

666

2,588

1,601

2,106

82

156

(2,153)

6,338

196

o.w. non-controlling interests

(4)

-

506

297

30

25

165

132

697

454

Group net income

1,492

666

2,082

1,304

2,076

57

(9)

(2,285)

5,641

(258)

Cost-to-income ratio

72.5%

74.1%

51.8%

55.1%

72.0%

88.2%

68.2%

75.6%

Average allocated capital*

11,149

11,427

10,246

10,499

14,916

14,302

16,324

15,860

52,634

52,091

RONE (businesses)/ROTE (Group)

13.4%

5.8%

20.3%

12.4%

13.9%

0.4%

11.7%

-0.4%

*Amounts adjusted compared with the financial statements published in 2020 (See Note1.7 of the financial statements).

-

2.4 NEW IMPORTANT PRODUCTS OR SERVICES

2.4.1 SOCIETE GENERALE ISSUES THE FIRST STRUCTURED PRODUCT ON PUBLIC BLOCKCHAIN

On 15 April 2021, Societe Generale issued the first structured product(1) as a Security Token directly registered on the Tezos public blockchain. The securities were fully subscribed by Societe Generale Assurances. The operation follows in the footsteps of a first covered bond Security Token issuance worth EUR 100 million on the Ethereum blockchain, settled in euros in April 2019, and of a second covered bond Security Token issuance worth EUR 40 million, this time settled in Central Bank Digital Currency (CBDC) and issued by Banque de France in May 2020. This latest transaction completes a new step in the development of Societe Generale – Forge, a regulated subsidiary of Societe Generale Group, which aims to offer crypto assets structuring, issuing, exchange and custody services to the Group’s professional clients by 2022.

This new experimentation, performed in accordance with best market practices, demonstrates the legal, regulatory and operational feasibility of issuing more complex financial instruments (structured products) on public blockchain. It leverages this disruptive technology which enables increased efficiency and fluidity of financial transactions: unprecedented product structuration capacity, shortened time-to-market, automated corporate actions, increased transparency and transaction and settlement speeds, as well as reduced cost and fewer intermediaries.

Thanks to Societe Generale – Forge’s innovative operating model, Security Tokens can be directly integrated into conventional banking systems interfaced with the SWIFT format. Innovation is key to Societe Generale Group’s digital transformation. The Group has been involved for several years in numerous initiatives based on blockchain and distributed ledger technologies, using the most innovative technologies and creating disruptive business models, with the aim of better serving its clients.

-

2.5 ANALYSIS OF THE CONSOLIDATED BALANCE SHEET

(In EURbn)

31.12.2021

31.12.2020

Cash, due from central banks

180.0

168.1

Financial assets at fair value through profit or loss

342.7

429.5

Hedging derivatives

13.2

20.7

Financial assets at fair value through other comprehensive income

43.5

52.1

Securities at amortised cost

19.4

15.6

Due from banks at amortised cost

56.0

53.4

Customer loans at amortised cost

497.2

448.8

Revaluation differences on portfolios hedged against interest rate risk

0.1

0.4

Investments of insurance companies

178.9

166.9

Tax assets

4.8

5.0

Other assets

92.9

67.3

Non-current assets held for sale

0.0

0

Investments accounted for using the equity method

0.1

0.1

Tangible and intangible fixed assets

32.0

30.1

Goodwill

3.7

4.0

TOTAL

1,464.5

1,462.0

(In EURbn)

31.12.2021

31.12.2020

Due to central banks

5.2

1.5

Financial liabilities at fair value through profit or loss

307.6

390.2

Hedging derivatives

10.4

12.5

Due to banks

135.3

135.6

Customer deposits

139.2

456.1

Debt securities issues

509.1

139.0

Revaluation differences on portfolios hedged against interest rate risk

2.8

7.7

Tax liabilities

1.6

1.2

Other liabilities

106.3

84.9

Non-current liabilities held for sale

0.0

-

Insurance contract related liabilities

155.3

146.1

Provisions

4.8

4.8

Subordinated debt

16.0

15.4

Shareholder’s equity

65.1

61.7

Non-controlling interests

5.8

5.3

TOTAL

1,464.5

1,462.0

2.5.1 MAIN CHANGES IN THE CONSOLIDATION SCOPE

The main changes to the consolidation scope at 31 December 2021 compared with the scope applicable at the closing date of 31 December 2020 are as follows:

On 31 December 2021, the Group finalised with Amundi the transfer of the asset management activities performed by Lyxor. This transfer concerns the passive (ETF) as well as active (including alternative) asset management activities performed by Lyxor on behalf of institutional customers in France and abroad; it includes the commercial and support functions dedicated to these activities.

This transfer resulted in a EUR 0.4 billion decrease in the Group’s total balance sheet including the EUR 223 million decrease in goodwill allocated to the Asset and Wealth Management CGU.

-

2.6 FINANCIAL POLICY

The objective of the Group’s financial policy is to optimise the use of shareholders’ equity in order to maximise short- and long-term return for shareholders, while maintaining a level of capital ratios (Common Equity Tier 1, Tier 1 and Total Capital ratios) consistent with the market status of Societe Generale and the Group’s target rating.

Since 2010, the Group has launched a major realignment programme, strengthening capital and focusing on the rigorous management of scarce resources (capital and liquidity) and proactive risk management to apply the regulatory changes related to the implementation of new Basel III regulations.

2.6.1 GROUP SHAREHOLDERS’ EQUITY

Group shareholders’ equity totalled EUR 65.1 billion at 31 December 2021. Net asset value per share was EUR 68.72 and net tangible asset value per share was EUR 61.08 using the new methodology disclosed in Chapter 2 of this Universal Registration Document, on page 46. Book capital includes EUR 8.0 billion in deeply subordinated notes.

At 31 December 2021, Societe Generale held, directly or indirectly, 22.2 million Societe Generale shares, representing 2.61% of the capital (excluding shares held for trading purposes). In 2021, no transaction was executed on purchases and sales under the liquidity contract concluded on 22 August 2011 with an external investment services provider.

-

2.7 MAJOR INVESTMENTS AND DISPOSALS

The group maintained a targeted acquisition and disposal policy, in line with its strategy focused on its core businesses and the management of scarce resources.

Business division

Description of investments

2021

International Retail Banking and Financial Services

Acquisition of Fleetpool, a leading German car subscription company.

International Retail Banking and Financial Services

Acquisition of Banco Sabadell’s subsidiary (Bansabadell Renting) specialised in long-term renting and the signing of an exclusive white label distribution agreement with Banco Sabadell.

International Retail Banking and Financial Services

Acquisition by ALD of a 17% stake in Skipr, a start-up specialised in mobility as a service.

2020

International Retail Banking and Financial Services

Acquisition of Reezocar, a French platform specialised in the online sale of used cars to individuals.

French Retail Banking

Acquisition of Shine, the neobank specialised in the professional and SME segments.

International Retail Banking and Financial Services

Acquisition of Socalfi, entity specialised in consumer credit in New Calendonia.

French Retail Banking

Acquisition by Franfinance of ITL, the equipment leasing company specialised in the environmental, manufacturing and healthcare sectors.

2019

International Retail Banking and Financial Services

Acquisition of Sternlease by ALD (fleet leasing in the Netherlands).

Global Banking and Investor Solutions

Acquisition of Equity Capital Markets and Commodities activities from Commerzbank.

French Retail Banking

Acquisition of Treezor, pioneering Bank-As-A-Service platform in France.

Business division

Description of disposals

2021

Global Banking and Investor Solutions

Disposal of Lyxor, a European asset management specialist

2020

International Retail Banking and Financial Services

Disposal of SG Finans AS, an equipment finance and factoring company in Norway, Sweden and Denmark.

International Retail Banking and Financial Services

Disposal of Société Générale de Banque aux Antilles.

International Retail Banking and Financial Services

Disposal by ALD of its entire stake in ALD Fortune (50%) in China.

Global Banking and Investor Solutions

Disposal of the custody, depository and clearing activities in South Africa.

2019

International Retail Banking and Financial Services

Disposal of SKB Banka in Slovenia.

International Retail Banking and Financial Services

Disposal of Pema GmbH, a truck and trailer rental company in Germany.

International Retail Banking and Financial Services

Disposal of its majority stake in Ohridska Banka SG in Macedonia.

International Retail Banking and Financial Services

Disposal of SG Serbja in Serbia.

International Retail Banking and Financial Services

Disposal of SG Montenegro.

International Retail Banking and Financial Services

Disposal of Mobiasbanka in Moldova.

International Retail Banking and Financial Services

Disposal of Inora Life en Ireland.

International Retail Banking and Financial Services

Disposal of Eurobank in Poland.

Global Banking and Investor Solutions

Disposal of SG Private Banking in Belgium.

French Retail Banking

Disposal of SelfTrade Bank S.A.U. in Spain.

French Retail Banking

Disposal of the entire stake in La Banque Postale Financement (35%).

International Retail Banking and Financial Services

Disposal of SG Express Bank in Bulgaria.

International Retail Banking and Financial Services

Disposal of SG Albania.

-

2.9 PROPERTY AND EQUIPMENT

The gross book value of Societe Generale Group’s tangible operating fixed assets amounted to EUR 45.7 billion at 31 December 2021. The figure comprises land and buildings (EUR 5.4 billion), the right of use (EUR 3.2 billion), assets leased by specialised financing companies (EUR 31.1 billion) and other tangible assets (EUR 6 billion).

The net book value of tangible operating assets and investment property amounted to EUR 29.2 billion, representing only 2% of the consolidated balance sheet at 31 December 2021.

-

2.10 POST-CLOSING EVENTS

On 6 January 2022, the Group announced the signing by Societe Generale and ALD of two Memorandums of Understanding under which ALD would acquire 100% of LeasePlan from a consortium led by TDR Capital. The proposed transaction is expected to close by the end of 2022.

On 1 February 2022, Societe Generale announced that Boursorama had signed a Memorandum of Understanding (MOU) with ING to offer ING’s online banking customers in France the best alternative banking solution, with adedicated customer journey and support conditions. The two parties intend to reach a final agreement by April 2022.

On 3 March 2022, Societe Generale issued an update on the Group’s situation in Ukraine and Russia. Societe Generale continues a detailed monitoring of the situation in Russia and Ukraine and is supporting its clients and all its employees to the highest degree possible.

Societe Generale is also rigorously complying with all applicable laws and regulations and is diligently implementing the measures necessary to strictly enforce international sanctions as soon as they are made public.

■its exposure(1)to Russia is limited at 1.7% of the Group’s total exposure, i.e. EUR 18.6 billion at 31 December 2021, of which EUR 15.4 billion (i.e. 83%) are accounted for at its subsidiary Rosbank;

■in 2021, activities located in Russia generated 2.8% of Group net banking income and 2.7% of Group net earning(2);

■the Group is extremely prudent and selective in the conduct of its activities in Russia and its priorities are focused to reduce its risks and preserve its subsidiary’s liquidity, while maintaining diversified deposit inflows;

■with a CET1 ratio of 13.7% at 31 December 2021, i.e. a buffer of around 470 basis points above the regulatory capital requirement, the Group has more than enough buffer to absorb the consequences of a potential extreme scenario, in which the Group would be stripped of property rights to its banking assets in Russia, with a capital impact estimated at around -50 basis points of the CET1 ratio and no effect on the payment of the dividend for the year 2021.

(1)“Exposure at default” on- and off-balance sheet on Russian counterparties, Russian subsidiaries or counterparties whose assets are mainly located in Russia, excluding counterparty risk on market operations whose current amount is limited.

The Group is following with the utmost attention the development of the situation in Ukraine and Russia, and it is committed to supporting its clients and all its employees. Societe Generale complies rigorously with legislation in force and diligently applies all necessary measures to strictly observe international sanctions as soon as they become public.

At Group level, the exposure to Russia(1) represents 1.7% of total exposure, i.e. EUR 18.6 billion at 31 December 2021 based on exchange rates at that date. The amount breaks down as: EUR 15.4 billion of exposure recognised in SG Russia(2) (“onshore exposures”) and EUR 3.2 billion recognised outside Russia (“offshore exposures”), of which EUR 2.6 billion on the balance sheet.

Group activities situated in Russia (SG Russia(2)) represent 2.8% of Group net banking income in 2021 and 2.7% of Group net income(3). They chiefly involve our banking subsidiary Rosbank, which is 99.97%-owned by the Group. Rosbank has a solid capital position, with a CET1 ratio of 10.74%, i.e. 274 basis points above the local regulatory requirement, and functions independently in terms of liquidity, with a loan-deposit ratio around 80% at 31 December 2021. These exposures are largely denominated in local currency, i.e. up to 99.7% on retail and 68% on corporate.

■retail outstandings account for approximately 41% of SG Russia’s(2) total exposure. They are 70%- secured (mortgage and auto loans), the remaining 30% of which mainly comprises loans to employees of Rosbank’s corporate clients, for whom the Bank processes their salaries;

■corporate exposure represents around 31% of the total and principally involves large Corporates (80%);

■russian sovereign debt and that of assimilated entities stands at EUR 3.7 billion, including around EUR 1.2 billion in sovereign bonds.

The Group is conducting its business in Russia with the utmost caution and selectivity, while supporting its historical clients. Its priorities are to reduce its risks and preserve the liquidity of its subsidiary by maintaining a diversified collection of deposits. The rouble clearing business is conducted entirely from Rosbank on behalf of the Group’s major clients.